What is GST ?

GST is an indirect tax that will bring together most of the INDIRECT taxes together that are imposed on all goods and services except a few under a single banner. This is in contrast to the current system where number of taxes levied separately on goods and services.

Now, guys the explanation I gave above is the one you will find everywhere written, but we need to know this topic thoroughly, like what it is, how will it work, what will it cover, benefits of it, drawbacks of it, and etc. etc. So, let’s come to the point, WHY we need GST in our system ?

PURPOSE OF VAT:

At present, we have sales tax system in states, it means the number of times a value is being added to the product, material or service, sales tax will be levied on it. (value addition –>> tax imposition)

let’s understand it by an example.

Suppose, Siddharth is a mobile dealer, who purchased a mobile phone worth Rs. 10,000. On this purchase he has paid 10% sales tax from his pocket i.e. Rs. 1000/- .

Now, he placed that phone in a box, pasted some stickers on it, you can say added some extra things worth Rs. 500.

Now, he sold that phone to Ms. Billa, now guys tell me, how much amount she has to pay to Siddharth ?

She has to pay…

10% on 10,000 (original cost) –>> 1000/-

10% on 500 (value added material) –>> 50/-

10% on 1000 (sales tax which was paid by Sidhharth) –>> 100/-

total tax –>> 1000 + 50 + 100 = 1150/-

Why sales tax was bad ?

- cascading effect

- tax on tax

- sell without bill (to avoid tax)

- bribe the inspectors

- black money will increase

- fiscal deficit will increase (due to less revenue collection)

Now, see third point, in which Ms. Billa has to pay 10% tax on 1000/- tax paid by Sidharth, this tax paid by Ms. Billa is paid on already paid tax, called TAX on TAX, also known as CASCADING effect.

The most important role of implying GST is to remove this cascading effect, which will eventually benefit the end consumer, here Ms. Billa, as now she dont have to pay this tax on tax she will save her Rs. 100/-.

After VAT/GST, she has to pay tax only of 1050/-. This is how the cascading effect will be removed.

VAT system has this input credit system.

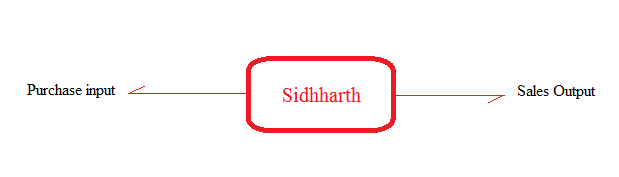

Dealer’s VAT Liability = sales output – purchase input

In this case, GST one, Sidhharth has paid 1000/- while purchasing that will be his purchase input and received 1050/- from Ms. Billa, that will be his sales output. So, his VAT liabilty will be, 1050-1000 = 50/- (this 50/- only he have to pay it to the state government)

This equation here means, the 1000/- tax money he paid he received back and the remaining 50/- will be his liablity.

See, another case. Here’s another mobile dealer Mr. Harry, suppose in year 2015.He puchased items worth some money and paid sales tax of 10,000/- on them, but due to some reasons he sold 50% of the items only and received 5.000/- tax only. So, in this case his VAT liability will be as this,

5000-10000 = -5000

Now, he will get account with a TIN number (tax identification number) also called tax ID, which will be having 5000/- as input credit at present.

Now, in 2016 Mr. Harry didnt purchased any item but sold the remaining 50% of the items and received 7000/- amount as sales tax. Now, his VAT liability would be,

7000-5000=2000

(means the 5000 earlier he had in his account, will be deducted from that acount, and he have to pay only 2000/- to the government as sales tax.)

Guys you getting my point, in 2015 Mr. Harry paid extra tax, was not his loss, that was recovered in 2016 when he sold the rest of the items. So, this is how the salesman will also be benefited from this tax implementation.

Let’s see the benefits of applying this tax now:

- tax evasion will be reduced

- government’s tax collection will increase

- fiscal deficit will reduce

- inflation can be controlled

- as all shopkeepers have to sell each item with bill/invoice, the policemen who used to take bribe in exchange of doing no enquiry for the shopkeepers selling items without paying bill to reduce tax burden will also reduce.

Now, see INTER-STATE trade (central sales tax):

lets say, ABC is a manufacturing company, which manufactures rubber,, it will manufacture rubber and pay EXCISE duty to central government. Now, tires are being made from that manufactured rubber, again company has to pay excise duty to central government. And now, Tony car making company, makes a car using this tires and will pay again excise duty to central government.

Now, this is again scene of TAX on TAX, cascading effect.

Solution: provide input credit to every person on every stage for the taxes he has already paid to the previous party, this will be done by MODVAT (modified VAT, only applied to central excise duty on goods only).

PROBLEM with MODVAT, other services used in manufacturing of car, such as colouring pattern, designing which Tony co. used from some foreign party and paid service tax to that party, but MODVAT system dont cover this part of service tax, so cascading effect was still present there and hence a new system was brought into system CENVAT (central VAT), this will provide input credit on both goods and services.

DRAWBACKS of VAT:

- electricity, fuel, advertisement on all these Sidhharth has to pay tax again on these items to state government and won’t get any input credit on these as these things are not included on VAT regime, and again cascading effect was there.

- Different VAT rates across different states.

- Different rates on different items.

- States demands cess, surcharge.

- To avoid tax, false invoicing will be in practice.

Why GST instead of VAT???

- services are not being covered in VAT.

- Input credit for all inputs is not being provided by VAT.

- Uniform rates are not there in VAT system, plus cess, surcharge extra.

What GST will do ???

- will cover both goods and services.

- Will cover most of the indirect taxes of both state and centre.

- Most of cess, surcharge will eliminate.

- Minimum exemptions.

- Some developed countries who have implied this GST tax, their revenue collection has increased and GDP also improved, exports increased also.

GST will be implimented on???

At central level.

All indirect taxes like, manufacturing tax, excise duty, cess, surcharge, services tax… all will come under CGST (central GST).

At state level.

All indirect taxes like, VAT, cess, surcharge etc. will come under SGST (state GST).

In case of inter- state trade, IGST will be implimented (integrated GST), this IGST is not the classification of GST, its just a system.

Proper products on which GST will be applied are not being decided by GOI yet.

GST will subsumes what ???

At central level

taxes at central level not come under GST.

- custom duty

- IGST on imported products.

- Cess on custom duty.

- Tobacco products, GST will be applicable on them, but excise duty also.

- Petroleum products right now not included in GST, only after government decides so.

Taxes of centre will come under GST.

- central excise duty.

- Central sales tax.

- Service tax.

- Special additional duty of customs (SAD).

- Toiletry preparation products with alcohol.

- Cess, surcharge on above items.

At state level

Taxes of state will not come under GST.

- excise duty on liquor for human consumptions.

- Stamp duty on immovable property.

- Electricity cess and duty.

- Petroleum products (only after GST council declares).

Taxes of state will come under GST.

- State VAT.

- Luxury tax.

- Purchase tax.

- Entertainment tax.

- Lottery, betting, gambling.

Before GST and After GST scenario…

Drawbacks of GST in India…

- doesn’t include Petroleum and alcohol products in it’s coverage.

- tax sharing between centre and states is another a bottleneck issue.

- very high GST rate.

- who all have to register for to get TIN number.

Reference: mrunal.org and other sites.

DO LET US KNOW WHAT YOU THINK ABOUT THIS ARTICLE. PLEASE PUT YOUR SUGGESTION UNDER COMMENT BOX BELOW. IN CASE YOU ARE NOT GETTING ANY POINT PLEASE ASK US.