What is a Bank Cheque?

Bank Check – A cheque is a negotiable instrument, as it can be transferred from one person to another and also it is precisely defined in the Negotiable Instruments Act, 1881. It is a written unconditional order addressed to a Banker to pay a certain sum of money to the person whose name is specified on it or to the bearer.

There are 3 parties involved in the Cheque:

- Drawer: The person who issues or writes the cheque.

- Drawee: It is the bank which would make the payment of the Cheque.

- Payee: Person to whom the payment of the cheque is made.

Types of check:

- Crossed Cheque: Any check that is crossed by two parallel lines, either across the whole check or through the top left-hand corner of the check. This crossing of the check means that the check can only be deposited directly into a bank account and cannot be immediately cashed by a bank or any other credit institution.

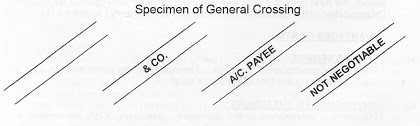

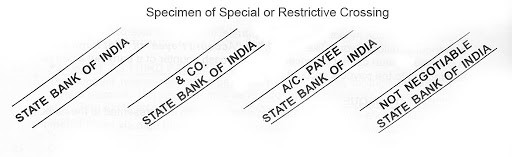

Types of crossing:

GENERAL crossing: the Check bears two parallel crossed lines simply, or in between them there is written “& Co.”/ “not negotiable”/”A/c. Payee”, that crossing will be called general crossing.

SPECIAL or RESTRICTIVE crossing: When a Bank’s name is also written between the parallel lines, this is called special crossing.

- Open check: The check which is not being crossed is called Open check. The payment of this check can be made by taking cash from the bank (won’t include any account by account transfer).

- Order check: Words “or Bearer” written on the check is cancelled, the check is called Order Check. The payment of this check can only be made to the person whose name is specified on it. This type of check is more secure.

- Bearer Check: if words “or Bearer” is not cancelled, the check is called Bearer Check. The payment of this check can be made to any person whether his/her name is mentioned on it or not.

- Local check: It is the check which is acceptable in the bank from where it is issued. Or to the bank which is connected to it. Or in the same city only.

- Post-dated Check: If the check is handed over before the date which is specified or, written on it, till that date, the check is called Post Dated Check.

- At- Par Check/ multicity Check: It is the check which is acceptable in all the cities across the country.

- Mutilated Check: A check which is torn into pieces, disfigured, burnt, eaten by insects is called mutilated check.

- Travellers Check: The check which is issued by the Bank for travelling purposes and it can be cashed from the bank after completing the journey. As it is risky to carry cash at the time of journey so as to reduce the risk, bank issues travellers check. It is in the form of a denomination.

- Bankers Check: It is the check which is issued by the Bank for itself. It is generally accepted in the same city and similar to Demand Draft.

Post-dated, Anti-dated and Stale/ outdated check:

Let today is 4 June 2015, and Ram issued a check and written date of 15 June 2015 on it. Check issued today will be called Post dated check, i.e. issued before date. And after 15 June 2015 that check will be called Anti-dated check, as it was issued before the date written on that, and after the period of 3 months, when the check will be expired, will be known as the Stale/outdated check.

Differences between Check and Demand Draft:

|

Cheque |

Demand Draft |

| 1. A check is issued by an individual. | It is issued by Bank. |

| 2. It is the Negotiable Instrument and it is precisely defined in the Negotiable Instruments Act,1881. | It is also a Negotiable Instrument but not precisely defined in the Negotiable Instrument Act,1881. |

| 3. A check is issued by an account holder of the Bank. | Demand Draft is issued by one of Branch of a Bank for another branch of the same Bank. |

| 4. Drawer and Drawee are different persons. | Drawer and Drawee are the same banks. |

| 5. Check can be dishonoured in case of insufficient funds. | It cannot be dishonoured. |

| 6. Payment of check can be stopped by the Drawer. | Payment of Demand Draft cannot be stopped. |

| 7. A check can be issued either as a bearer/order. |

Demand Draft can always be issued as an order. |

Check Truncation System :

- In India, it started in 2010.

- Under this system, Banks takes an electronic image of a check and sends it for clearing.

- CTS stopped the physical movement of a check from one Bank to another.

- Through CTS, check clearance process becomes speedy.

- It solved the problem of :

- Frauds

- Check misplacement (While clearing of the Check).